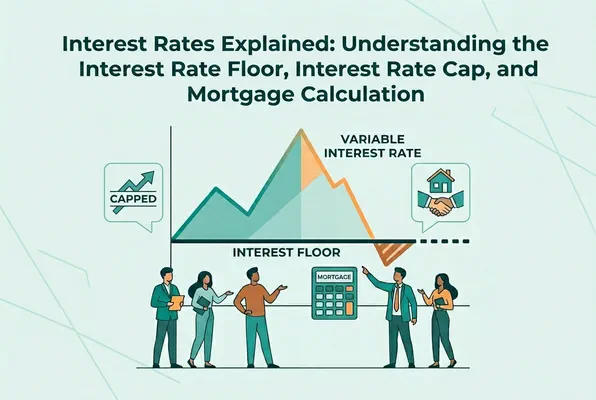

Interest Rate Floor Explained

Interest floors are one of the most misunderstood mechanisms in personal finance and commercial lending. You might have noticed a clause buried deep in your loan agreement stating something like “the interest rate shall not fall below 2.00%,” and wondered what that actually means for your wallet. Whether you are managing a mortgage, a business credit facility, or a student refinancing product, understanding how interest floors work gives you real power at the negotiating table and sharper insight into the true cost of borrowing.

This guide breaks down the mechanics, the motivations behind them, and practical strategies to minimize their impact on your financial life.

What Is an Interest Floor?

An interest floor—sometimes called a rate floor or minimum rate—is a contractual lower boundary on the interest rate applied to a variable-rate financial product. It guarantees that, regardless of how low the underlying benchmark rate falls, the lender will always collect at least the floor rate from the borrower.

Think of it as a safety net stretched beneath the interest rate: the rate can swing freely above it, but it can never fall through.

Interest floors appear across a wide range of financial products:

- Adjustable-rate mortgages (ARMs)

- Variable-rate personal loans

- Business lines of credit

- Syndicated corporate loans

- Interest rate derivatives and swap contracts

The Mechanics Behind the Number

Most variable-rate loans are priced as a benchmark rate plus a spread. For example:

Loan rate = SOFR + 2.50%, subject to a floor of 3.00%

If SOFR is currently 1.00%, your theoretical rate would be 3.50%—well above the floor, so the floor is irrelevant. But if SOFR drops to 0.25%, your theoretical rate would be 2.75%, which is below the 3.00% floor. In that scenario, you pay 3.00%, not 2.75%. The floor has just activated, costing you an extra 25 basis points.

This distinction—when a floor is dormant versus when it is binding—is crucial for understanding its real economic impact.

Interest Rate Caps and Floors in Modern Lending

In today’s financial system, an interest rate cap is often used alongside a floor and cap structure to define a protected range of rates for variable lending products. This combination, sometimes referred to as a cap and floor, ensures that borrowing costs remain within predefined boundaries. While the cap limits how high rates can rise, the floor provision establishes a minimum interest rate, preventing returns or payments from dropping below a certain level.

Why Lenders Use Interest Floors

Lenders are not arbitrary when they write floor clauses into contracts. There are clear financial, regulatory, and operational reasons behind the practice.

Protecting Net Interest Margins

A bank’s core revenue model depends on the spread between what it pays depositors and what it earns from borrowers—the net interest margin (NIM). When benchmark rates collapse, as they did during the 2008 financial crisis and again in 2020, a bank with many variable-rate loans can see its NIM compressed dangerously. A floor guarantees a minimum income stream, protecting the institution’s profitability and, by extension, its solvency.

Covering Operational and Credit Costs

Every loan carries costs: origination expenses, servicing fees, credit risk provisions, and regulatory capital requirements. These costs do not disappear when market rates fall. An interest floor ensures the lender at least covers these baseline costs even in an extreme low-rate environment.

Matching Funding Costs

Banks often fund loans with fixed-cost deposits or wholesale funding instruments. If the rate they charge borrowers can fall freely while funding costs remain sticky, the bank could end up in a loss position on individual loans. Floors prevent this mismatch from becoming catastrophic.

Regulatory Capital Incentives

Under Basel III and related frameworks, banks must hold capital against credit exposures. A guaranteed minimum cash flow from a floored loan can improve the risk-adjusted return calculation, making the loan more attractive from a capital efficiency standpoint.

How Interest Floors Work in Different Loan Types

The mechanics are consistent in principle, but the implementation varies significantly depending on the product.

Adjustable-Rate Mortgages

In an ARM, the interest floor is often called the floor rate or sometimes confused with the initial rate. It is written into the promissory note and governs the minimum rate throughout the loan’s life.

For example, a 5/1 ARM might carry: - Initial rate: 4.50% - Margin: 2.75% - Index: 1-Year CMT - Caps: 2% periodic / 5% lifetime - Floor: 4.50% (equal to the initial rate)

In this structure, the floor equals the starting rate, meaning the borrower can never benefit from a rate reduction below where they started. This is a common—and somewhat controversial—practice in mortgage lending.

Business Lines of Credit

Commercial lenders frequently use SOFR (Secured Overnight Financing Rate) or the Prime Rate as their benchmark. A business line of credit might read:

Rate = Prime + 1.00%, minimum 5.50%

During the COVID-19 era, when the Fed cut rates aggressively, many small businesses discovered their variable-rate lines were actually floored and not adjusting downward as expected. Understanding this clause in advance would have allowed better cash flow planning.

Student Loan Refinancing

Private student loan refinancers often embed floors within their variable-rate products. These floors are sometimes set based on the lender’s internal cost of capital and may not be prominently advertised. Borrowers comparing fixed versus variable options should always ask: “What is the rate floor, and at what index level does it become binding?”

Interest Rate Derivatives

In the derivatives world, an interest rate floor is actually a standalone financial instrument—a contract that pays the holder the difference between the floor rate and the reference rate when the reference rate falls below the floor. These are used by:

- Borrowers to hedge against the cost of embedded floors in their loans

- Lenders to offset the income loss from loans without floors

- Investors seeking income in low-rate environments

Each payment period in such a contract is called a floorlet, and the collection of floorlets constitutes the floor instrument. Pricing uses models similar to options pricing, particularly variants of the Black model.

Interest Floors vs. Interest Caps vs. Collars

To fully understand how interest floors work, it helps to place them in context with related rate boundary mechanisms.

| Mechanism | Protects | Description |

|---|---|---|

| Interest Floor | Lender | Sets the minimum rate; borrower pays at least this amount |

| Interest Cap | Borrower | Sets the maximum rate; borrower pays no more than this |

| Interest Collar | Both | Combines a floor and a cap into a single structure |

The Interest Rate Collar

A collar is particularly common in commercial real estate and corporate finance. A borrower might accept a floor (protecting the lender) in exchange for a cap (protecting themselves). The two trade-offs effectively subsidize each other—a collar can sometimes be structured at zero net cost, where the premium of the cap is offset by the value of the floor sold to the lender.

Understanding this interplay gives sophisticated borrowers leverage: if a lender insists on a floor, a borrower can reasonably request a corresponding cap.

The Real Cost of an Interest Floor

Quantifying the actual cost of a floor requires looking at how often it is likely to be binding over the life of the loan—a concept borrowers almost never consider when signing.

Expected Cost Calculation

The expected cost depends on:

- Probability that the benchmark rate falls below the floor during the loan term

- Magnitude of the difference when it does

- Duration of the period during which the floor is binding

In mathematical terms, the value of a floor to the lender (and cost to the borrower) is analogous to a put option on the interest rate. When rates are volatile or trending downward, the floor has significant value. In a rising rate environment, floors are dormant and essentially costless.

Historical Context

From 2009 to 2015 and again from 2020 to 2022, benchmark rates were near historic lows. Borrowers with floored variable-rate loans discovered they were effectively paying fixed rates while believing they held flexible instruments. In some cases, borrowers paid 100–200 basis points more than they would have on an unflored variable product over multi-year periods.

Opportunity Cost

Beyond the direct payment difference, there is an opportunity cost: capital that goes toward excess interest payments cannot be deployed into savings, investments, or debt repayment. Over a 10-year loan at $250,000, an extra 1.50% annual cost due to a binding floor translates to approximately $37,500 in additional interest—a meaningful figure that underscores the importance of scrutinizing floor clauses.

How to Identify Interest Floors in Your Loan Documents

Floors are not always labeled with dramatic language. Here is what to look for.

Common Disclosure Phrases

- “The interest rate will not be less than [X]%”

- “Subject to a minimum rate of [X]%”

- “The floor rate is set at [X]%”

- “Notwithstanding the foregoing, the rate shall be no lower than [X]%”

- “The index rate shall be deemed to be at least [X]% for purposes of calculating the applicable rate”

Where to Look

- Promissory note: The primary legal document governing loan terms

- Loan agreement or credit agreement: Common in commercial lending

- Adjustable Rate Mortgage (ARM) disclosure: Required by Regulation Z / TILA in the US

- Product summary or Key Facts Document: Common in UK and EU regulated markets

Using Loan Calculators to Model Floor Impact

Tools like those available on finflexia.app allow you to model different rate scenarios and visualize when a floor becomes binding. By inputting the floor rate, the benchmark rate, and your loan balance, you can generate payment schedules that reveal the true cost under various economic conditions. This kind of scenario modeling is invaluable before committing to any variable-rate product.

Strategies for Borrowers to Minimize the Impact of Interest Floors

Once you understand how interest floors work, you can take proactive steps to reduce their impact on your borrowing costs.

1. Negotiate the Floor Rate Directly

Particularly in commercial lending, the floor rate is a negotiable term. Lenders set initial proposals based on standard models, not individual borrower characteristics. If you have strong credit, a long relationship with the institution, or substantial collateral, you have grounds to push back.

Ask specifically: “Can we lower the floor by 25 or 50 basis points in exchange for a higher margin spread or a prepayment commitment?” This kind of trade-off is common in sophisticated loan negotiations.

2. Compare Floored vs. Unfloored Products

Some lenders—especially online and fintech lenders—offer variable-rate products without explicit floors, or with floors set so low they are unlikely ever to be binding. Compare the all-in cost (spread + floor) across multiple lenders before deciding.

3. Choose Fixed Rates in Low-Rate Environments

When benchmark rates are low and the floor is likely to be binding for much of the loan term, a variable-rate loan offers little real flexibility. In such environments, locking in a fixed rate may actually cost less in practice while eliminating rate uncertainty.

4. Purchase an Interest Rate Floor Derivative

Larger borrowers—particularly businesses with significant floating-rate debt—can purchase standalone floor derivatives to offset the economic cost of embedded floors in their loans. While this adds complexity, it can be cost-effective at scale.

5. Refinance When Conditions Change

If you entered a loan when the floor was dormant but rates have since dropped below it, refinancing into a new product (potentially with a lower or no floor) can yield meaningful savings. Always factor in refinancing costs when calculating whether this makes financial sense.

6. Request Full Disclosure Before Signing

Before signing any variable-rate agreement, ask for a written statement of: - The exact floor rate - The benchmark index used - The margin above the benchmark - Historical performance of the benchmark over the past 10–20 years

This due diligence positions you to make an informed decision and signals to the lender that you are a sophisticated borrower.

Interest Floors in a Macroeconomic Context

Understanding how interest floors work is not just a personal finance exercise—it has macroeconomic implications that help explain central bank behavior and credit market dynamics.

The Zero Lower Bound Problem

Central banks historically assumed that benchmark rates could not go below zero—the so-called zero lower bound. Most loan floor clauses were written with this assumption in mind, setting floors at or near 0%. When European and Japanese central banks began implementing negative interest rate policy (NIRP), this created novel problems: could a lender pass negative rates through to borrowers? In most cases, floors prevented this, meaning borrowers did not benefit from negative-rate environments while lenders still collected their floor minimum.

Impact on Monetary Policy Transmission

When a large proportion of outstanding loans carry binding floors, monetary policy easing becomes less effective. Rate cuts by central banks do not translate into lower borrowing costs for floored borrowers, weakening the transmission mechanism. This is why central bankers monitor the prevalence of rate floors in the lending market as part of their policy toolkit assessment.

Post-LIBOR Transition Considerations

The global transition from LIBOR to alternative risk-free rates (RFRs) like SOFR, SONIA, and EURIBOR has introduced new floor dynamics. SOFR, being a near risk-free overnight rate, is structurally lower than LIBOR was for comparable maturities. This means floors that were dormant under LIBOR-based loans may become binding under SOFR-based repricing—a subtle but real cost increase for borrowers who did not anticipate this shift.

Interest Floors for Investors and Savers

The concept of interest floors is not limited to the borrower side of the equation. It appears in investment products as well.

Floored Floating Rate Notes

Some floating rate notes (FRNs) issued by corporations or governments include a floor on the coupon payment. From an investor’s perspective, this floor is beneficial—it guarantees a minimum income stream regardless of benchmark rate movements. This feature makes floored FRNs attractive in low-rate environments.

Structured Products

Many bank-issued structured notes, principal-protected products, and market-linked deposits incorporate floor mechanics to guarantee minimum returns. Understanding what the floor is, how it compares to simple savings alternatives, and what you give up in exchange is essential due diligence for retail investors considering these products.

Common Misconceptions About Interest Floors

Given their complexity, several persistent myths surround interest floors. Clearing these up can prevent costly misunderstandings.

Misconception 1: “A Floor Just Protects the Lender—It Has No Value to Me”

In some collar arrangements, accepting a floor can be exchanged for a cap that limits your maximum rate exposure. In this sense, a floor you “sell” to the lender has value that can be monetized into borrower protections.

Misconception 2: “Floors Are Only Relevant When Rates Are Very Low”

While floors are most often binding in low-rate environments, they can also become relevant during the adjustment period of a new loan, during local or regional economic downturns, or when a borrower’s loan is tied to an index that behaves differently from the broader market.

Misconception 3: “Fixed Rate Loans Don’t Have Floors”

True, fixed-rate loans don’t have rate adjustment mechanisms, but they embed a form of floor logic in their pricing: the lender has already accounted for the possibility of rate fluctuations and priced the loan accordingly. Understanding this pricing is equally important.

Misconception 4: “All Variable Rate Loans Have Floors”

Not all variable-rate products include explicit floors. Some lenders—particularly in competitive retail markets—offer unfloored variable rates to attract borrowers. These products can carry greater downside risk for the lender, which is often compensated through higher initial spreads.

Checklist: What to Ask Before Accepting a Variable-Rate Loan

Use this checklist to ensure you fully understand the floor mechanics before signing:

- What is the exact floor rate on this loan?

- What benchmark index is used, and what is its current level?

- At what benchmark level does the floor become binding?

- Has the floor ever been binding on this type of product historically?

- Is there also an interest cap that protects me on the upside?

- Can the floor rate be negotiated?

- How is the floor disclosed in the loan documentation?

- What is the estimated cost of the floor over the full loan term using current rate forecasts?

Conclusion

Understanding how interest floors work transforms you from a passive borrower into an informed financial decision-maker. Floors are not inherently bad—they serve legitimate purposes in lending markets and even provide value to investors in certain structured products. But they can carry significant hidden costs that only become visible when rates fall sharply.

The key takeaways are straightforward: always identify the floor in any variable-rate product, model the cost across different rate scenarios, negotiate where possible, and choose between fixed and floored variable rates based on the realistic probability of the floor being binding during your loan term.

Tools like those on finflexia.app make this scenario modeling accessible, helping you visualize rate paths and compare total loan costs before committing. In a world where lending agreements run to dozens of pages of fine print, knowing exactly what an interest floor does—and when it kicks in—may be one of the most valuable pieces of financial literacy you can develop.

Written by

Dominik KonoldFounder

Dominik is the founder of Finflexia and an expert in treasury accounting, financial instrument valuation and IFRS compliance. Since 2016, he's been a certified Professional Risk Manager (PRMIA) and also lectures for the Association of Public Banks and the Academy of International Accounting. He built Finflexia to help treasury teams automate complex accounting workflows.

Related Posts

Embedded Derivative Accounting: Complete Guide (IFRS 9 & ASC 815)

This guide explains embedded derivative accounting under IFRS and ASC 815, including fair value measurement, hybrid instrument assessment, and the closely related test.

Embedded Derivative: Identification, Separation & Accounting

This article explains embedded derivatives under ASC 815 and IFRS, including how to identify, separate, and account for them. It also outlines when a derivative under ASC 815 must be bifurcated and how it impacts financial reporting.

IFRS 9 Financial Instruments: Complete Guide

This Guide provides a comprehensive overview of IFRS 9, explaining its classification and measurement rules, expected credit loss model, hedge accounting requirements, and its interaction with IFRS 7 and other IFRS standards.

Ready to simplify your treasury accounting?

See how Finflexia helps you manage financial instruments with ease. Book a demo to learn more.

Book a Demo