Embedded Derivative Accounting: Complete Guide (IFRS 9 & ASC 815)

Embedded derivative accounting sits at one of the most technically demanding intersections in financial reporting. It combines derivative valuation, contract analysis, and judgment-intensive classification decisions — all under the watchful eye of auditors and standard-setters who have refined their guidance significantly over the last decade.

Whether you are a treasury professional managing structured notes, a financial controller reviewing convertible bond arrangements, or an auditor evaluating a client’s hybrid instruments, understanding the mechanics of embedded derivative accounting is not optional. It is essential.

This guide walks you through everything you need to know: what embedded derivatives are, how to identify them, when bifurcation is required, how IFRS 9 and ASC 815 differ, and how modern tools can make the entire process more reliable and efficient.

What Is an Embedded Derivative?

An embedded derivative is a component embedded within a host contract that causes some or all of the cash flows of that combined instrument — often called a hybrid instrument or hybrid contract — to vary in a way that is similar to a standalone derivative.

The host contract itself can be a wide range of financial or non-financial arrangements:

- A debt instrument (e.g., a bond with an interest rate cap or floor)

- An equity instrument (e.g., convertible notes)

- A lease agreement (e.g., with rent indexed to commodity prices)

- A purchase or sale contract (e.g., priced in a foreign currency that is neither party’s functional currency)

- An insurance contract

- A service agreement with variable pricing tied to inflation indices

The embedded component behaves like a derivative because its value changes in response to changes in an underlying variable — such as an interest rate, commodity price, foreign currency exchange rate, credit rating, or equity index — but it cannot be separately traded or transferred from the host contract.

Common Examples of Embedded Derivatives

| Host Contract | Embedded Derivative Feature |

|---|---|

| Fixed-rate bond with equity conversion option | Equity conversion option |

| Floating-rate debt with interest rate floor | Interest rate floor (a type of option) |

| Commodity purchase contract priced in USD (non-USD entity) | FX forward element |

| Inflation-linked lease payments | Inflation swap element |

| Credit-linked notes | Credit default swap element |

| Callable bonds | Call option on interest rates |

Understanding these examples is the first step toward accurate embedded derivative accounting. The challenge lies in whether any given embedded feature must be separated (bifurcated) from its host and accounted for as a standalone derivative at fair value.

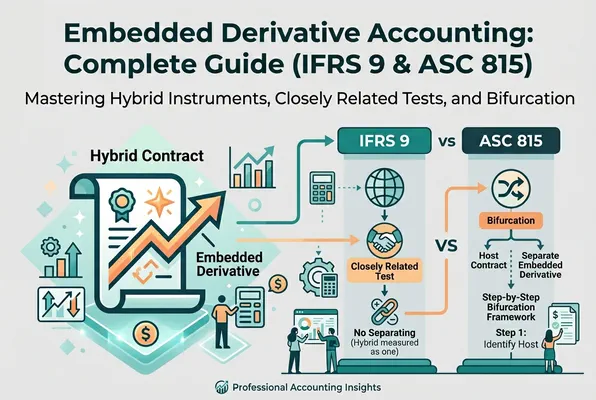

The Regulatory Framework: IFRS 9 vs. ASC 815

Two primary accounting standards govern embedded derivative accounting globally:

- IFRS 9 Financial Instruments (and residual references to IAS 39) — applicable to entities reporting under International Financial Reporting Standards

- ASC 815 Derivatives and Hedging — applicable to entities reporting under US GAAP

While both frameworks share a conceptual foundation, their specific rules — particularly regarding when bifurcation is required — differ in important ways.

Accounting treatment of embedded derivatives in practice

In practice, accounting for embedded derivatives begins with the definition of a derivative instrument, since this determines whether a feature within an instrument or contract qualifies for separation under the relevant accounting guidance, including ASC 815-15-25-1. The initial accounting treatment depends on whether the contract is assessed as a single unit or whether it contains multiple embedded derivatives that must be evaluated independently. Where conditions are met, the embedded feature is separated from its host contract and accounted for separately, with the host contract and the embedded derivative following different measurement models. In such cases, the embedded component is typically accounted for as derivatives and reported at fair value, with changes often recorded in earnings under fair value through earnings. Complex structures involving embedded forward or swap features or option-based embedded elements require further judgment to determine whether an embedded derivative would meet bifurcation criteria and is therefore considered an embedded derivative. Ultimately, proper recognition and measurement ensures consistent treatment across both the host instrument and any embedded components embedded within it.

IFRS 9: The Dominant Global Standard

IFRS 9, effective for annual periods beginning on or after 1 January 2018, fundamentally restructured how embedded derivatives in financial assets are treated. Rather than requiring embedded derivative analysis for financial assets, IFRS 9 mandates that the entire hybrid financial asset be classified and measured as a whole.

The classification is driven by two tests:

- Business Model Test: Is the financial asset held to collect contractual cash flows, held to collect and sell, or held for other purposes?

- SPPI Test (Solely Payments of Principal and Interest): Do the contractual cash flows of the instrument represent solely payments of principal and interest on the outstanding principal amount?

If a hybrid financial asset fails the SPPI test because of its embedded feature, the entire instrument is measured at fair value through profit or loss (FVTPL). There is no separate accounting for the embedded derivative component.

This was a deliberate simplification designed to reduce complexity and increase consistency.

Important exception: For financial liabilities and non-financial host contracts under IFRS 9, the old IAS 39 bifurcation logic still applies. This means the three-condition test (described below) remains highly relevant for:

- Convertible bonds issued by the entity

- Structured notes payable

- Commodity supply contracts with pricing mechanisms linked to unrelated indices

- Lease contracts with variable payments tied to non-lease-related indices

ASC 815: The US GAAP Approach

Under ASC 815, embedded derivative accounting applies to both financial and non-financial host contracts. The framework requires bifurcation of an embedded derivative when all three of the following conditions are met:

- The economic characteristics and risks of the embedded derivative are not clearly and closely related to the economic characteristics and risks of the host contract

- The hybrid instrument is not remeasured at fair value with changes in fair value reported in current earnings

- A separate instrument with the same terms as the embedded derivative would be a derivative instrument subject to ASC 815

ASC 815 also includes a long list of scope exceptions and implementation guidance covering specific types of embedded features — making it one of the most voluminous sections of US GAAP.

The Bifurcation Decision: A Step-by-Step Framework

The core question in embedded derivative accounting is often: should I bifurcate? Here is a structured approach to making that determination, applicable under both IFRS (for financial liabilities and non-financial contracts) and US GAAP.

Step 1: Identify the Host Contract

First, determine the nature of the host contract. Is it:

- A financial liability (e.g., a borrowing, a note payable)?

- A financial asset (handled differently under IFRS 9, as discussed)?

- A non-financial contract (e.g., a purchase agreement, lease, insurance policy)?

The nature of the host contract affects which guidance applies and how the closely related test is evaluated.

Step 2: Identify Potential Embedded Features

Review the full terms and conditions of the contract. Look for provisions that cause cash flows to vary based on:

- Changes in interest rates or credit spreads

- Commodity prices

- Foreign exchange rates

- Equity or index prices

- Inflation indices unrelated to the entity’s operating environment

- Credit events or rating changes

Not every variable payment makes something an embedded derivative. Payments that vary based on the counterparty’s performance (like a revenue-sharing clause) are generally not derivatives. The key is a financial underlying that is separate from the substance of the host contract.

Step 3: Apply the Closely Related Test

This is where professional judgment is most heavily exercised. The question is whether the risks and characteristics of the embedded feature are closely related to those of the host contract.

Examples where the embedded feature IS closely related (no bifurcation required):

- An interest rate cap or floor on a floating-rate debt instrument, if the cap/floor is at-the-money or out-of-the-money at inception

- An inflation-linked adjustment in a long-term contract where inflation is genuinely relevant to the performance of that contract

- A prepayment option in a debt instrument where the prepayment amount approximates amortized cost

Examples where the embedded feature is NOT closely related (bifurcation likely required):

- A conversion feature on a debt instrument into a fixed number of equity shares

- A commodity-price-linked return on a debt instrument (e.g., gold-indexed bonds)

- Foreign currency exposure in a non-financial contract where the foreign currency is neither the functional currency of either party nor a commonly used currency for that type of contract

- Leveraged interest rate features that multiply rate movements

Step 4: Check for FVTPL Election

If the entity has designated the entire hybrid instrument at fair value through profit or loss (which is permitted under both IFRS 9 and ASC 815 when certain conditions are met), bifurcation is not required. This election can simplify accounting significantly — though it comes with its own income statement volatility implications.

Step 5: Determine Measurement Basis if Bifurcation Is Required

When bifurcation is required:

- The embedded derivative is separated and measured at fair value, with changes recognized in profit or loss

- The host contract is accounted for under the applicable standard for that type of instrument (e.g., amortized cost for a debt host)

The fair value of the embedded derivative at inception is deducted from (or added to) the total consideration paid/received, with the residual allocated to the host contract.

Measurement and Fair Valuation of Embedded Derivatives

Once bifurcated, the embedded derivative must be measured at fair value at each reporting date. This requires:

Selecting an Appropriate Valuation Model

The valuation model depends on the nature of the embedded derivative:

- Options (caps, floors, conversion features): Black-Scholes model, binomial trees, or other option pricing models

- Forward/swap elements: Discounted cash flow models using relevant market forward curves

- Credit-linked features: Credit default swap pricing models or structural credit models

Key Inputs and Market Data Requirements

Reliable fair value measurement requires access to:

- Current yield curves and forward interest rate curves

- Volatility surfaces for options (implied volatility by strike and maturity)

- Credit spreads for the relevant issuer and instrument

- FX forward rates for currency-linked features

- Commodity forward prices for commodity-linked instruments

Under IFRS 13 and ASC 820, entities must classify their fair value measurements into the three-level hierarchy (Level 1, Level 2, Level 3) based on the observability of inputs. Most embedded derivatives will fall into Level 2 or Level 3, requiring careful documentation of valuation assumptions.

Day-One Gains and Losses

A particularly sensitive area in embedded derivative accounting is the treatment of day-one gains or losses. Where the fair value of the separated embedded derivative at initial recognition differs from zero (which can occur if the embedded derivative is in-the-money at inception), entities need to carefully evaluate whether this represents a genuine market value difference or an error in the bifurcation or valuation methodology.

Under IFRS, day-one gains for Level 3 instruments are generally deferred and recognized over the life of the instrument or when the instrument is derecognized. US GAAP has similar considerations.

Hedge Accounting and Embedded Derivatives

A natural question arises: can an embedded derivative that has been bifurcated be designated as a hedging instrument in a hedge accounting relationship?

Under both IFRS 9 and ASC 815, a bifurcated embedded derivative can generally be designated as a hedging instrument, provided the normal hedge accounting eligibility criteria are met:

- The hedging relationship must be formally documented

- The hedging instrument must be expected to be highly effective in offsetting the designated hedged risk

- The hedged item must meet eligibility requirements

However, there are nuances. Under IFRS 9, only derivatives (including bifurcated embedded derivatives) can be designated as hedging instruments in most hedge accounting relationships. Under ASC 815, the rules on what constitutes an eligible hedging instrument are similarly structured but differ in details.

It is also worth noting that an embedded derivative that has not been bifurcated (because the closely related test was passed) cannot generally be designated separately as a hedging instrument — you cannot designate something you have not separated.

Practical Challenges in Embedded Derivative Accounting

Finance professionals regularly encounter a set of recurring challenges when implementing embedded derivative accounting in practice.

Contract Review and Identification

The most common failure point is not identifying embedded derivative features in the first place. This often happens because:

- Legal contracts are reviewed by legal teams without derivative accounting lenses

- New contract templates are approved without accounting review

- Complex structured instruments are acquired without adequate due diligence on their embedded features

Best practice: Establish a cross-functional review process that includes treasury, accounting, and legal whenever new contracts are entered into that contain variable pricing, conversion rights, or cross-currency features.

Reassessment Triggers

Under both IFRS and US GAAP, the bifurcation assessment is generally made at inception and is not subsequently reassessed unless the contract is significantly modified. This means that:

- Renegotiated contracts may need to be re-evaluated from scratch

- Amendments that change the nature of variable payment features can create new embedded derivative assessments

- Novations and refinancings often reset the assessment clock

Intercompany and Intragroup Instruments

Intercompany loans, especially cross-border loans where the loan currency is neither party’s functional currency, are a frequent source of overlooked embedded derivatives. A USD-denominated intercompany loan between a USD-functional parent and a EUR-functional subsidiary creates an FX derivative embedded in the host debt instrument from the subsidiary’s perspective.

These instruments should be on every multinational group’s radar during both initial implementation and ongoing monitoring.

Documentation and Audit Evidence

Auditors will require robust documentation supporting:

- The identification of all hybrid instruments in scope

- The closely related analysis for each embedded feature

- The fair valuation methodology and key inputs

- Any FVTPL elections made

Maintaining a hybrid instrument register — a centralized log of all contracts containing potential embedded derivatives, along with the assessment conclusions and supporting analysis — is considered best practice.

Technology and Automation: Modernizing Embedded Derivative Accounting

Given the complexity and judgment intensity of embedded derivative accounting, finance teams are increasingly turning to purpose-built technology platforms to systematize the process.

Modern solutions like finflexia.app are designed to support treasury and accounting teams with:

- Systematic identification workflows that flag contracts for embedded derivative review based on configurable criteria

- IFRS 9 and ASC 815 classification logic built into the platform, guiding users through the bifurcation decision tree

- Automated fair value calculations using market data feeds for common embedded derivative types (interest rate options, FX forwards, commodity forwards)

- Hedge accounting documentation templates and effectiveness testing modules

- Audit-ready reporting with full calculation transparency and input documentation

The benefits of automation extend beyond accuracy. When embedded derivative accounting is handled through a structured platform, finance teams spend less time on mechanical assessments and more time on the judgment-intensive aspects of the work — leading to better accounting outcomes and more defensible positions.

Key Features to Look for in an Embedded Derivative Accounting Tool

When evaluating technology for embedded derivative accounting, consider:

| Feature | Why It Matters |

|---|---|

| Multi-standard support (IFRS 9 & ASC 815) | Essential for multinational groups |

| Integration with market data providers | Ensures fair values use current, observable inputs |

| Scenario and sensitivity analysis | Supports disclosure requirements under IFRS 7 and ASC 815-20 |

| Audit trail and version control | Critical for external audit and internal governance |

| Modular hedge accounting workflow | Enables seamless connection between embedded derivatives and hedging programs |

Disclosure Requirements

Both IFRS 7 and ASC 815 impose significant disclosure obligations for entities with embedded derivatives.

IFRS 7 Disclosures

Under IFRS 7, entities must disclose:

- The significance of financial instruments (including hybrid instruments) to their financial position and performance

- The nature and extent of risks arising from financial instruments, including those arising from embedded derivatives

- Quantitative information about exposure to interest rate risk, currency risk, and other market risks — all of which can be affected by embedded derivative features

- Fair value disclosures, including the level in the fair value hierarchy and a description of the valuation technique and inputs used

ASC 815-20 Disclosures

Under US GAAP, ASC 815 requires disclosures about:

- The location and fair value of derivative instruments in the balance sheet (including bifurcated embedded derivatives)

- The effect of derivative instruments on the income statement

- The volume of derivative activity

- Credit risk concentrations associated with derivative instruments

For embedded derivatives specifically, entities must disclose the fair value of the embedded derivative and its host contract, and the changes in fair value recognized in earnings.

Transition and Implementation Considerations

For entities first implementing IFRS 9 or transitioning from IAS 39, the embedded derivative accounting rules deserve careful attention during the transition process.

Retrospective vs. Modified Retrospective Application

IFRS 9 permitted entities to apply either:

- Full retrospective application: Restate all prior periods as if IFRS 9 had always applied

- Modified retrospective approach: Apply the new requirements from the date of initial application without restating comparatives

For entities with significant portfolios of hybrid financial instruments, the classification and measurement outcomes under IFRS 9 versus IAS 39 can differ substantially — particularly where hybrid financial assets were previously bifurcated under IAS 39 but are now measured at FVTPL in their entirety under IFRS 9.

Day-One Differences and Opening Retained Earnings

Where the IFRS 9 classification of a hybrid financial asset differs from the prior IAS 39 treatment, the difference in carrying amounts is recognized in opening retained earnings at the transition date. This can result in material adjustments to equity for entities with significant structured financial asset portfolios.

Summary: Key Principles for Getting Embedded Derivative Accounting Right

Embedded derivative accounting is complex, but it is manageable when approached systematically. Here are the core principles to keep in mind:

- Identification comes first: You cannot account for what you have not found. Build robust processes to identify hybrid instruments across all contract types.

- Know your standard: IFRS 9 has largely eliminated bifurcation for financial assets, but the old rules remain for financial liabilities and non-financial hosts. ASC 815 applies broadly across financial and non-financial contracts.

- The closely related test requires judgment: Invest time in understanding the economic substance of the embedded feature relative to the host contract. Consult examples in the standards and application guidance.

- Fair value measurement demands rigour: Use appropriate models, observable inputs where possible, and document your valuation methodology thoroughly.

- FVTPL election can simplify: Where eligible, designating the entire hybrid instrument at FVTPL eliminates the need for bifurcation and can reduce accounting complexity — though income statement volatility must be considered.

- Leverage technology: Modern platforms like finflexia.app can systematize identification, classification, and measurement — reducing risk and freeing finance professionals to focus on judgment-intensive decisions.

- Document everything: Auditors will scrutinize embedded derivative accounting. Maintain a hybrid instrument register, bifurcation analysis files, valuation workings, and any FVTPL election documentation.

The standards governing embedded derivative accounting will continue to evolve as financial products grow in complexity. Staying current with IFRS and FASB guidance, investing in the right tools, and building institutional knowledge across finance and treasury teams are the foundations for sustainable, high-quality financial reporting in this area.

Written by

Dominik KonoldFounder

Dominik is the founder of Finflexia and an expert in treasury accounting, financial instrument valuation and IFRS compliance. Since 2016, he's been a certified Professional Risk Manager (PRMIA) and also lectures for the Association of Public Banks and the Academy of International Accounting. He built Finflexia to help treasury teams automate complex accounting workflows.

Related Posts

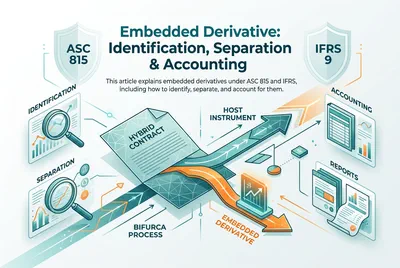

Embedded Derivative: Identification, Separation & Accounting

This article explains embedded derivatives under ASC 815 and IFRS, including how to identify, separate, and account for them. It also outlines when a derivative under ASC 815 must be bifurcated and how it impacts financial reporting.

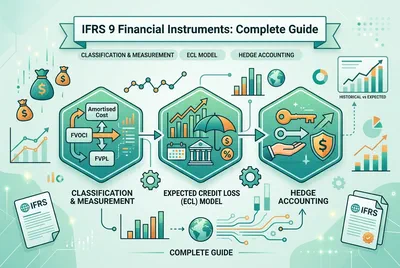

IFRS 9 Financial Instruments: Complete Guide

This Guide provides a comprehensive overview of IFRS 9, explaining its classification and measurement rules, expected credit loss model, hedge accounting requirements, and its interaction with IFRS 7 and other IFRS standards.

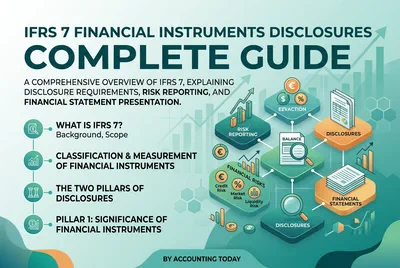

IFRS 7 Financial Instruments Disclosures: Complete Guide

This Guide provides a comprehensive overview of IFRS 7, explaining its disclosure requirements for financial instruments, risk reporting, and presentation in financial statements.

Ready to simplify your treasury accounting?

See how Finflexia helps you manage financial instruments with ease. Book a demo to learn more.

Book a Demo