Convertible Loans Explained: Understanding Convertible Debt and Convertible Notes in Modern Financing

A convertible loan has become one of the most widely used financing instruments in the startup world — and for good reason. It offers a fast, flexible way to raise early-stage capital without the complexity of immediately agreeing on a company valuation. Whether you are a founder seeking seed funding or an investor looking for an entry point into a promising startup, understanding how convertible loans work is essential.

This guide breaks down everything you need to know: the mechanics, the key terms, the advantages, the risks, and how to use a convertible loan effectively in 2026.

What Is a Convertible Loan?

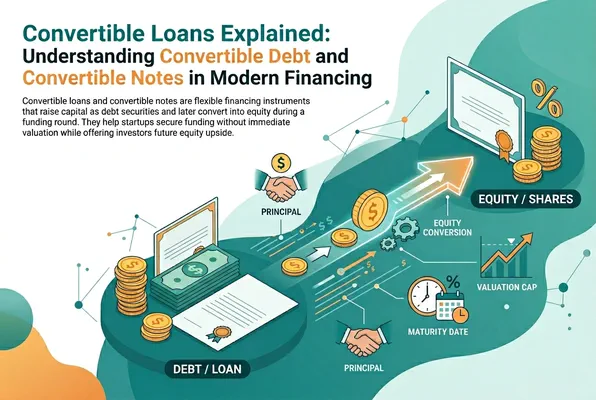

A convertible loan (also called a convertible note) is a short-term debt instrument that is designed to convert into equity at a later date — typically when the company raises a qualifying funding round. Unlike a traditional bank loan, the primary intention is not repayment but conversion into shares.

Here is the core dynamic: an investor lends money to a startup today. Instead of receiving regular interest payments and a lump-sum repayment at maturity, the investor expects to receive equity in the company once a predefined trigger event occurs. The outstanding principal — and often the accrued interest — converts into shares at that point.

This structure makes a convertible loan fundamentally different from both a standard loan and a direct equity investment. It sits somewhere in between, combining characteristics of debt and equity.

How a Convertible Loan Differs from Traditional Debt

In a traditional loan, the lender is primarily interested in being repaid with interest. The borrower’s business success is relevant only to the extent that it determines creditworthiness. In a convertible loan, the investor actively wants the company to grow, because conversion into equity becomes far more valuable if the startup succeeds.

How a Convertible Loan Differs from Direct Equity Investment

In a direct equity investment, the investor purchases shares at an agreed valuation. This requires a negotiated price per share and a formal valuation of the company — a process that can be time-consuming and contentious, especially for very early-stage startups where valuation is largely speculative.

A convertible loan defers this valuation discussion to a future round, when more data is available. This is one of its most significant practical benefits.

Key Terms Every Founder and Investor Must Know

Understanding the mechanics of a convertible loan requires familiarity with a handful of essential terms. These provisions define the economics and the risk-reward profile of the instrument.

Principal Amount

The principal is the amount of money the investor lends to the startup. This is the face value of the convertible loan and forms the baseline for conversion calculations.

Interest Rate

Most convertible loans carry an annual interest rate, typically between 4% and 10%. Unlike a standard loan, this interest usually does not result in periodic cash payments. Instead, it accrues over the life of the loan and is added to the principal at the time of conversion. This means the investor receives slightly more equity than the raw principal amount would suggest.

In some jurisdictions, a minimum interest rate is legally required to avoid the loan being reclassified as a hidden equity contribution. Always consult legal counsel on this point.

Maturity Date

The maturity date is the deadline by which the convertible loan must either convert into equity or be repaid. Typical maturity periods range from 12 to 24 months. If a qualifying funding round has not occurred by the maturity date, the parties must decide whether to repay the loan, extend the maturity, or trigger a conversion at an agreed valuation.

A looming maturity date can create tension between founders and investors, particularly if fundraising is taking longer than expected.

Valuation Cap

The valuation cap is arguably the most investor-friendly provision in a convertible loan. It sets a maximum pre-money valuation at which the loan can convert into equity, regardless of the actual valuation achieved in the next funding round.

Example: Suppose an investor provides a convertible loan with a valuation cap of €5 million. The startup later raises a Series A at a pre-money valuation of €20 million. Without a cap, the investor’s loan would convert at €20 million, giving them a relatively small equity stake. With the €5 million cap, the investor’s loan converts at €5 million — giving them four times as many shares as they would otherwise receive.

The valuation cap rewards early investors who took on significantly more risk than later-stage investors.

Discount Rate

The discount rate gives convertible loan investors the right to convert their loan at a lower price per share than the investors in the qualifying funding round. A typical discount is between 10% and 30%.

Example: If Series A investors pay €10 per share, and the convertible loan carries a 20% discount, the convertible loan holder converts at €8 per share. This provides an additional reward for the risk taken at an earlier, more uncertain stage.

When both a valuation cap and a discount rate exist in the same convertible loan, the investor typically benefits from whichever mechanism produces the more favorable conversion price.

Qualifying Financing Round

This term defines exactly what kind of fundraising event triggers an automatic conversion. Usually, it is a funding round above a minimum threshold — for example, a Series A of at least €1 million or €2 million. This threshold prevents trivial funding events from triggering conversion at unfavorable terms.

Most Favored Nation (MFN) Clause

An MFN clause protects early investors by ensuring that if the startup issues subsequent convertible loans with better terms (e.g., a higher discount or lower valuation cap), the original investor can upgrade their terms to match. This is particularly relevant when a startup raises multiple convertible loans over time.

Convertible Debt and Equity Financing in Modern Funding Structures

Convertible debt is a widely used form of debt financing that sits between straight debt and equity financing. It is a financial instrument that allows investors to provide capital in the form of loans that can later convert to equity under specific conditions. This process is often defined in a term sheet, where key terms in a convertible structure such as valuation cap, discount, and maturity are agreed. Instruments like convertible loan notes, convertible bonds, and other debt securities are commonly used to raise capital while preserving flexibility compared to traditional equity. Instead of immediate dilution like in traditional equity or equity funding, investors receive the option to convert their investment into shares at a conversion price is the price agreed upon in a future round of funding or subsequent funding round.

How the Conversion Process Works

The conversion of a convertible loan into equity follows a defined sequence of events. Understanding this process helps both founders and investors avoid misunderstandings and disputes.

Step 1: The Trigger Event Occurs

Most commonly, the trigger is a qualifying financing round. When a startup closes a funding round above the minimum threshold defined in the convertible loan agreement, conversion becomes mandatory (or at the investor’s option, depending on the agreement).

Step 2: Calculating the Conversion Price

The conversion price is determined by applying the valuation cap and/or discount rate to the price per share paid by new investors in the qualifying round. The investor receives shares at whichever price is more favorable.

Step 3: Converting Principal and Accrued Interest

The amount that converts is typically the original principal plus any accrued but unpaid interest. This accrued interest effectively increases the investor’s equity stake at conversion.

Step 4: Issuing New Shares

The startup issues new shares to the convertible loan investor, diluting existing shareholders (including the founders). This dilution is the cost of the early-stage capital.

What Happens at Maturity Without Conversion?

If the maturity date arrives and no qualifying round has occurred, several outcomes are possible:

- Repayment: The startup repays the principal plus accrued interest in cash.

- Extension: Both parties agree to extend the maturity date.

- Conversion at a negotiated valuation: Both parties agree on a valuation and convert the loan into equity without a formal funding round.

- Default: If the startup cannot repay and no agreement is reached, the investor may have legal recourse, though in practice this often means writing off the investment.

How Debt Converts Into Equity

In most cases, the debt that converts or known as convertible instruments will convert the debt or convert the note into shares once a subsequent funding round occurs. At this point, the debt converts into equity, meaning the investor can convert their loan into equity or see the note converts to equity, resulting in a loan into shares mechanism. This process is often described as debt conversion or simply convertible debt financing, where debt into equity happens automatically or under specific conditions. The resulting shares are typically treated as equity, which can lead to equity dilution for existing shareholders, as the equity at a future date is shared with new investors.

Advantages of a Convertible Loan

The popularity of the convertible loan in the startup ecosystem is not accidental. It offers concrete benefits to both founders and investors.

For Founders

Speed and simplicity. A convertible loan can be structured and closed in days or weeks, compared to months for a priced equity round. Less legal complexity means lower transaction costs.

No immediate valuation negotiation. Valuation at the pre-seed or seed stage is highly uncertain. Deferring this discussion until a later round — when more traction and data are available — helps founders avoid being undervalued at the earliest and most critical stage.

Flexibility. Convertible loans can be structured with a high degree of flexibility around amounts, timelines, interest rates, and conversion triggers.

Maintaining control. Since a convertible loan does not immediately issue new shares, founders retain their current ownership percentage and voting rights until conversion.

For Investors

Downside protection. As a debt instrument, a convertible loan sits higher in the capital structure than equity. In the event of insolvency, debt holders are prioritized over equity holders. This provides a degree of protection that a direct equity investment does not offer.

Upside through the cap and discount. The valuation cap and discount rate ensure that early investors are compensated for their risk with a better-than-market price at conversion.

Faster deployment. The speed of execution means investors can deploy capital quickly and begin building their position in promising startups without lengthy negotiations.

Risks and Challenges of Convertible Loans

While the convertible loan is a powerful tool, it is not without risks. Both parties should approach it with a clear understanding of what can go wrong.

For Founders

Dilution uncertainty. Because the number of shares issued at conversion depends on the future valuation, founders cannot precisely calculate how much dilution they will experience when signing a convertible loan. A very high valuation cap or large discount in a stagnant market could result in severe dilution.

Maturity pressure. If the startup has not closed a qualifying round by the maturity date, the founder faces pressure to either repay the loan in cash (which most early-stage startups cannot afford) or negotiate an extension under potentially unfavorable terms.

Multiple convertible loans stacking up. Many startups raise multiple convertible loans sequentially. As these stack up, the aggregate dilution at conversion can be greater than founders anticipated — sometimes leading to a “dilution cliff” at the first priced round.

Interest accrual. Unlike equity, a convertible loan accrues interest. This increases the amount that converts and therefore the dilution for founders.

For Investors

No guaranteed return. Despite its debt characteristics, a convertible loan in a startup context is not a safe investment. If the startup fails before a qualifying round, investors may receive little or nothing.

Conversion terms may erode value. If the valuation cap is set too high or the discount is too low, early investors may not receive adequate compensation for the risk they took.

Illiquidity. Convertible loan positions cannot be easily transferred or sold. Investors must typically wait for a conversion event or maturity to realize any return.

Convertible Loan vs. SAFE vs. Equity Round: Choosing the Right Instrument

Choosing the right funding instrument depends on the stage of the company, the jurisdiction, the investor’s preferences, and the strategic goals of both parties.

Convertible Loan vs. SAFE

The SAFE (Simple Agreement for Future Equity), pioneered by Y Combinator, is the American cousin of the convertible loan. Key differences:

| Feature | Convertible Loan | SAFE |

|---|---|---|

| Debt instrument | Yes | No |

| Interest | Yes (typically) | No |

| Maturity date | Yes | No |

| Repayment obligation | Yes (if no conversion) | No |

| Common jurisdiction | Europe, global | US-centric |

SAFEs are simpler and have no repayment obligation, which is favorable for founders. However, convertible loans provide investors with debt protections that SAFEs do not — making them more common in European markets where investors prefer the additional security layer.

Convertible Loan vs. Priced Equity Round

A priced round (e.g., Series A) involves a full company valuation, the issuance of shares at a defined price, and often the negotiation of investor rights such as board seats, liquidation preferences, and anti-dilution protections. This is more rigorous and more expensive to execute, but it provides complete clarity on ownership and governance from day one.

For very early-stage companies, a convertible loan is usually faster and cheaper. For companies raising above €2–5 million with institutional investors, a priced round may make more sense.

Legal and Structural Considerations

Jurisdiction Matters

The legal treatment of convertible loans varies significantly by country. In Germany, for example, convertible loans must be carefully structured to avoid reclassification as a “shareholder loan” (Gesellschafterdarlehen), which would subordinate the investor’s claim in insolvency. In the UK and US, the legal frameworks are generally more flexible.

Always engage a startup-experienced lawyer when drafting a convertible loan agreement, regardless of jurisdiction.

Standard Documentation

Many startup ecosystems have developed standard convertible loan templates to reduce legal costs and speed up execution. In Europe, organizations such as the British Business Bank and various accelerators have published model agreements. Using standardized documents reduces negotiation time and helps both parties understand the standard market terms.

Cap Table Management

Every convertible loan creates a contingent claim on the company’s equity. Founders must maintain an up-to-date cap table that accounts for all outstanding convertible loans, their potential conversion scenarios, and the resulting dilution. Failure to do so can create unpleasant surprises at the time of a priced round.

Modern cap table management tools, including those available at finflexia.app , can model convertible loan conversion scenarios and give founders a clear picture of post-conversion ownership under different assumptions.

Best Practices for Structuring a Convertible Loan

Whether you are a founder or an investor, the following principles will help you structure a convertible loan that is fair, functional, and future-proof.

For Founders

- Set the valuation cap thoughtfully. A cap that is too low will result in excessive dilution at conversion. Use current comparable transactions to benchmark an appropriate cap.

- Keep the maturity date realistic. Choose a maturity period that gives you enough runway to close a qualifying round — typically 18 to 24 months.

- Limit the number of outstanding convertible loans. Multiple notes with different terms can create significant complexity and dilution at conversion. Try to consolidate where possible.

- Model your dilution scenarios. Before signing, model the worst-case and best-case conversion scenarios to understand the potential impact on your cap table.

For Investors

- Negotiate a meaningful valuation cap. The cap should reflect your assessment of the company’s fair value at the time of investment, plus a buffer for risk.

- Include an MFN clause. If the startup raises additional convertible loans later, an MFN clause ensures you are not disadvantaged relative to later investors.

- Conduct proper due diligence. The speed of a convertible loan does not eliminate the need for due diligence. Understand the business model, the team, and the market before committing capital.

- Understand the maturity provisions. Know exactly what happens at maturity and ensure the agreement gives you adequate options if a qualifying round does not occur in time.

The Role of Convertible Loans in the Startup Funding Lifecycle

A convertible loan is rarely the only funding instrument a startup uses. It typically plays a specific role in the early stages of the funding lifecycle.

Pre-Seed and Seed Stage

At the pre-seed and seed stage, a startup often has little more than an idea, a prototype, and a founding team. Valuation is highly speculative. A convertible loan allows founders to raise initial capital from friends, family, or angel investors without the complexity of a priced round.

Bridging to the Next Round

A convertible loan is also commonly used as a bridge instrument — a way to extend a startup’s runway while it prepares for its next priced funding round. For example, a startup that has closed its seed round and is preparing for a Series A might raise a bridge convertible loan to fund operations for an additional 6–12 months.

Strategic Use in Down Rounds

In challenging market conditions, some investors agree to convert or extend a convertible loan rather than triggering a formal down round (where new shares are issued at a lower valuation than previous rounds). This can protect existing investors from aggressive anti-dilution provisions while giving the startup time to recover.

Convertible Loan in 2026: Market Trends

The convertible loan remains a cornerstone of early-stage startup financing in 2026. Several trends are shaping how it is being used:

- Increasing standardization. More accelerators and early-stage venture funds are using standardized convertible loan templates, reducing legal costs and negotiation friction.

- AI-assisted cap table modeling. Tools that automatically model convertible loan conversion scenarios are becoming standard for founders managing complex cap tables.

- Cross-border complexity. As startups raise from international investors, the interaction between different jurisdictions’ legal treatments of convertible loans is creating new challenges — and demand for expert guidance.

- Rising interest rates impact. In a higher interest rate environment, the interest provisions in convertible loans have become more material. Both founders and investors are paying closer attention to how accrued interest affects conversion economics.

Advantages and Disadvantages of Convertible Structures

The advantages of convertible instruments and specifically the advantages of convertible loan include speed, flexibility, and the ability to delay valuation discussions while allowing startups to raise funding efficiently. They often offer favourable terms for early investors compared to bank debt, venture debt, or other forms of debt funding, since they include the option to convert into potential equity at a later stage. However, there are also disadvantages of convertible structures, such as uncertainty around dilution and valuation. The final value of the convertible bond depends on the present value of future equity, making outcomes harder to predict compared to debt securities or fixed repayment structures. For founders, this means carefully managing how and when they issue convertible instruments, since poorly structured deals can significantly impact ownership after a round of funding or equity funding event.

Conclusion

The convertible loan is a versatile, founder-friendly, and investor-protective instrument that has earned its place as one of the most important tools in early-stage startup financing. By deferring the valuation question, protecting investors with debt-like features, and rewarding early risk-taking through caps and discounts, the convertible loan balances the interests of all parties in a way that few other instruments can.

Understanding the mechanics — the principal, interest, maturity date, valuation cap, discount rate, and conversion triggers — is essential for anyone involved in startup finance. Equally important is understanding the risks: dilution uncertainty for founders, illiquidity for investors, and the potential for tension at maturity.

Used correctly and structured thoughtfully, a convertible loan can be the bridge that takes a startup from an early idea to a fundable, scalable business — and that gives early investors the returns they need to justify their risk.

For tools to model your convertible loan scenarios and manage your cap table with confidence, explore what finflexia.app has to offer.

Written by

Dominik KonoldFounder

Dominik is the founder of Finflexia and an expert in treasury accounting, financial instrument valuation and IFRS compliance. Since 2016, he's been a certified Professional Risk Manager (PRMIA) and also lectures for the Association of Public Banks and the Academy of International Accounting. He built Finflexia to help treasury teams automate complex accounting workflows.

Related Posts

Convertible Bond: Complete Guide for Investors

Convertible bonds are hybrid securities that combine fixed income with equity upside, allowing investors to earn interest and convert into shares of common stock under defined conditions.

Derivative Accounting: IFRS 9 & ASC 815 Complete Guide

A complete guide to derivative accounting: explore types of derivatives, fair value measurement, hedge accounting, and financial reporting under IFRS and US GAAP.

Modern Treasury Management Software for Smarter Financial Operations

Learn how treasury management software improves treasury operations by centralizing financial data, enhancing visibility, automating processes, and optimizing cash and liquidity management within a modern treasury management system.

Ready to simplify your treasury accounting?

See how Finflexia helps you manage financial instruments with ease. Book a demo to learn more.

Book a Demo